- Return to Article Of The Month index

2018 Mid-Year U.S. Cattle Inventory Report

September, 2018

Chris Prevatt,

UF/IFAS Range Cattle Researh and Education Center, Ona

The semi-annual U.S. Cattle Inventory Report was released on July 20, 2018 by the National Agricultural Statistics Service (NASS). This report provides a brief update relative to July 1st inventories for U.S. breeding stock, feeder cattle, and calves with a comparison against the previous year’s mid-year report.

| Table 1. U.S. Cattle Inventory, July 1, 2017 and 2018 | ||||

| Class | 2017 | 2018 | Change | |

| (mil. head) | (mil. head) | (mil.head) | % | |

| Total Cattle (all Cattle and Calves) | 102.2 | 103.2 | 1.0 | 1.0% |

| All Cows | 41.6 | 41.9 | 0.3 | 0.7% |

| Beef Cows that Calved | 32.2 | 32.5 | 0.3 | 0.9% |

| Heifers, 500 lbs. & over | 16.2 | 16.3 | 0.1 | 0.6% |

| Beef Replacement Heifers | 4.7 | 4.6 | -0.1 | -2.1% |

| Other Heifers, 500 lbs. & over | 7.3 | 7.5 | 0.2 | 2.7% |

| Steers, 500 lbs. & over | 14.5 | 14.5 | 0.0 | 0.0% |

| Calves, under 500 lbs. | 27.9 | 28.4 | 0.5 | 1.8% |

| Calf Crop | 35.8 | 36.5 | 0.7 | 2.0% |

| Feeder Cattle and Calf Supply | 36.9 | 37.1 | 0.2 | 0.5% |

| U.S. Cattle on Feed, All Sizes | 12.8 | 13.3 | 0.5 | 3.9% |

| Source: USDA-NASS | ||||

The Total Cattle Inventory (All Cattle and Calves) in the U.S.

as of July 1, 2018 totaled 103.2 million head, increasing by 1.0

million head (1.0%) above the 102.2 million head on July 1,

2017. All cows and heifers that have calved totaled 41.9 million

head, increasing by 300,000 head (0.7%). The nation’s beef cow

herd (Beef Cows that Calved) continues to grow totaling 32.5

million head, which was an increase of 300,000 head (0.9%) above

July 1, 2017.

Heifers, 500-pounds and over totaled

16.3 million head, an increase of 100,000 head (0.6%) above last

year. One of the significant findings from this report was that

the number of beef replacement heifers retained declined below

year ago levels, down 100,000 head (-2.1%). Steers, 500-pounds

and over remained unchanged compared to a year ago totaling 14.5

million head. Bulls, 500-pounds and over totaled 2.1 million

head, an increase of 100,000 head (5.0%) from July 2017. Calves,

under 500-pounds totaled 28.4 million head, an increase of

500,000 head (1.8%) compared with July 1, 2017. The 2018 U.S.

Calf Crop is expected to be 36.5 million head, increasing by

700,000 head (2.0%) from last year’s calf crop. Feeder Cattle

and Calf Supply totaled 37.1 million head, increasing by 200,000

head (0.5%). The Feeder Cattle and Calf Supply is the combined

total of calves under 500 pounds and other heifers and steers

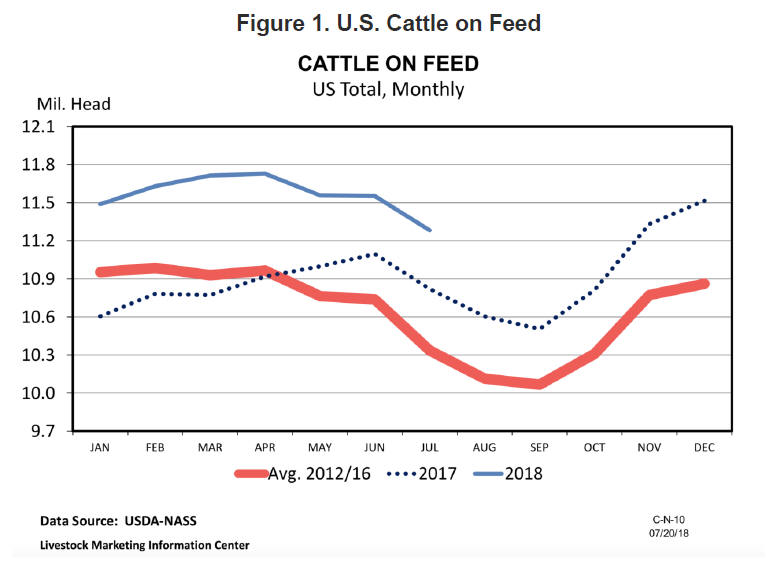

over 500 pounds (outside of feedlots). The U.S. Cattle on Feed,

All Sizes (Figure 1) was 13.3 million head, increasing by

500,000 (3.9%) head from a year-ago. The July 1st

Cattle on Feed number is the largest mid-year cattle inventory

number since the data series began in 1996.

The results of the January 1st and July 1st cattle

inventory reports have made it clear that expansion is still taking place.

However, growth rates during the buildup phase of the U.S. cattle cycle

continue to decline. Regardless, there will be abundant supplies of cattle

for the next several years that will result in record levels of production.

These supplies of both beef and competing animal proteins will be a

price-limiting factor, despite strong domestic and global demand. Therefore,

continued beef herd expansion should continue to be viewed as moderately

bearish on cattle prices during the next couple of years. Remember, that

changes in cattle inventory will be slow due to the size of the beef

industry and the reproductive biology of cattle. Lastly, for producers

marketing their feeder calves during the fall 2018, note that there were an

additional 600,000 head of feeder calves were born during the first half of

2018 compared to 2017, thus the fall calf-run should continue to see growth

this year.